Uncovering the Pre-ECB Drift and Its Buying and selling Technique Functions

Because the world’s consideration shifts from the US-centric fairness markets to worldwide fairness markets (which strongly outperform on the YTD foundation), we may evaluation some fascinating anomalies and patterns that exist exterior of the USA. On the earth of financial coverage, merchants have lengthy noticed a notable constructive drift in U.S. equities on days surrounding Federal Reserve (FOMC) conferences. Curiously, an analogous—however barely shifted—sample emerges in European markets round European Central Financial institution (ECB) press conferences. Our quantitative evaluation reveals that European fairness markets are likely to exhibit a robust and constant upward drift on the day earlier than the ECB’s scheduled press convention. The explanation for this timing distinction lies in logistics: for the reason that ECB usually speaks at 14:15 CET (8:15 a.m. EST), properly earlier than the foremost U.S. markets open, traders typically front-run the potential market-friendly alerts from the central financial institution. Reasonably than danger holding positions into the uncertainty of the announcement itself, market individuals progressively construct up publicity the day earlier than, pricing in expectations of dovish or supportive coverage strikes.

In central banking, the European Central Financial institution (ECB) and the Federal Reserve (FED) play pivotal roles in shaping monetary markets by their financial insurance policies. The Federal Open Market Committee (FOMC) assembly impact, as documented by Quantpedia, highlights vital inventory value actions round FOMC bulletins, underscoring the affect of central financial institution selections on monetary markets. This text explores how markets reply to the European FED counterpart, the ECB, and its insurance policies, specializing in

the idea of drift—the tendency of asset costs to maneuver in a selected path over time—and

the skewness of returns, which displays the asymmetry in market reactions across the time of central financial institution bulletins.

Background

Central banks just like the ECB and the FED affect monetary markets by varied mechanisms, together with rate of interest changes and ahead steerage. The FOMC, specifically, has been studied extensively for its affect on inventory costs.

Analysis means that institutional traders exploit Fed leaks to commerce forward of FOMC conferences, resulting in knowledgeable buying and selling that may considerably affect market outcomes. Moreover, our in-house analysis discovered that calendar and seasonal anomalies, such because the FOMC assembly impact, could be mixed with different methods to boost profitability.

Methodology

We make use of a quantitative method to evaluate market value motion and return distributions prior, and following central financial institution coverage bulletins. The evaluation contains solely speedy reactions and short-term implications based mostly on market volatility attributable to anticipated ECB selections.

Knowledge

Our research analyzes the affect of ECB bulletins on

European indices such because the DAX and STOXX 50, alongside

the consequences of ECB selections on U.S. ETFs like FEZ (SPDR Euro Stoxx 50 ETF), VGK (Vanguard European Inventory Index Fund ETF), EWG (iShares MSCI Germany ETF), and HEDJ (WisdomTree Europe Hedged Fairness Fund) ETFs.

For all the ETF historic knowledge, we used knowledge from EODHD.com – the sponsor of our weblog. EODHD presents seamless entry to +30 years of historic costs and basic knowledge for shares, ETFs, foreign exchange, and cryptocurrencies throughout 60+ exchanges, accessible through API or no-code add-ons for Excel and Google Sheets. As a particular provide, our weblog readers can get pleasure from an unique 30% low cost on premium EODHD plans.

Financial coverage statements knowledge are sourced from the official ECB web site.

The primary one is from September 1998, coinciding with our DAX and EWG pattern begin.

The STOXX pattern begins in 2007,

VGK in 2005,

FEZ in 2002, and

HEDJ in 2010.

Market Reactions to ECB Bulletins

Preliminary findings point out that markets exhibit vital drift and volatility changes previous ECB coverage selections, which differ barely from the price-action round FED bulletins.

The magnitude of those results varies relying on the coverage announcement and the prevailing market circumstances. As an example, easing financial coverage shocks tends to elicit constructive market reactions, significantly amongst lively merchants and hedge funds near regional reserve banks. Nonetheless, we observe a notable phenomenon the place the drift is most pronounced not on the day of the ECB convention however on the day previous it. This may be attributed to the “purchase the rumor, promote the information” adage, the place market individuals alter their positions in anticipation of the announcement relatively than responding to it.

Visualizing Inventory Index Market Reactions

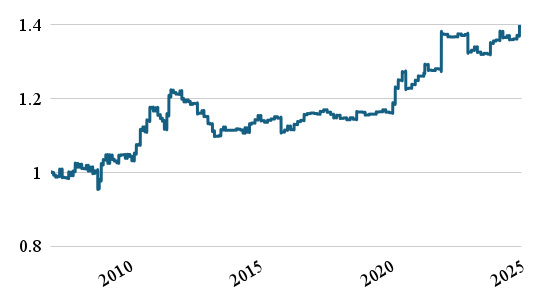

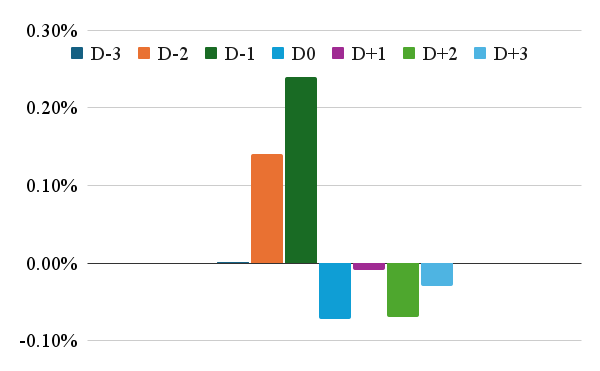

For instance these dynamics, we first current histogram charts for the DAX and STOXX 50 indices and fairness curves for D-1 positions (efficiency of the hypothetical buying and selling technique that buys DAX or STOXX 50 index on D-2 shut and sells index on the shut of D-1 day).

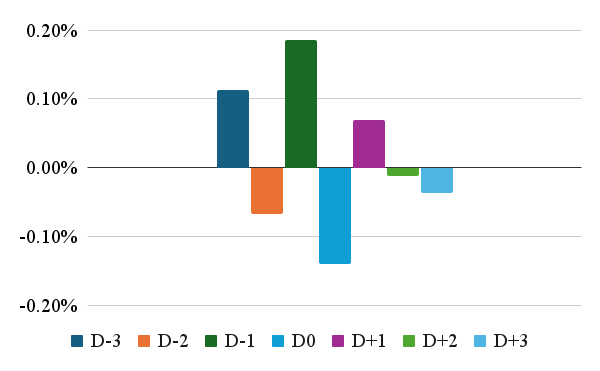

Distributions of Returns per Day of Previous and After ECB Conferences

We will see that returns on the day previous the convention are considerably constructive; can we make one thing out of it? Let’s proceed and and research the efficiency of D-1 fairness curves, highlighting the effectiveness of holding European inventory indices D-1 days earlier than ECB conferences.

These easy methods leverage the pre-announcement drift to generate constructive returns.

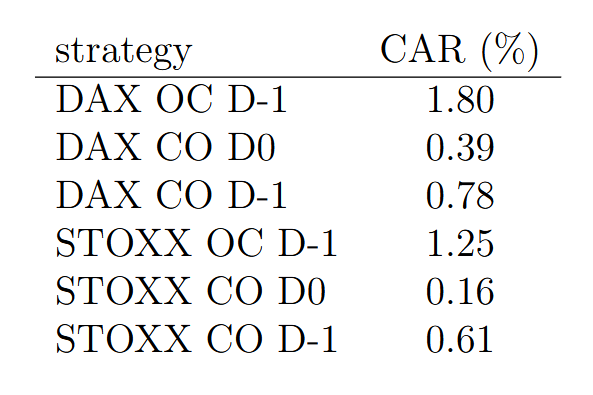

Classes Returns

Our additional evaluation entails dissecting these indices into Open-to-Shut (OC) and Shut-to-Open (CO) periods. To save lots of the area, we ppresent simply the DAX Index outcomes, because it appears essentially the most delicate to ECB selections. Nonetheless, the STOXX 50 Index motion patterns are very related. Our objective was to higher determine when the value motion happens—within the intraday (open-to-close) or in a single day (close-to-open) periods.

What’s the fundamental takeaway from our evaluation? We will observe that the pre-ECB drift happens throughout 3 totally different periods – Shut-to-Open session throughout the night time (from D-2 to D-1), then throughout the Open-to-Shut session within the D-1, and indexes have a nonetheless constructive efficiency throughout the Shut-to-Open session from D-1 to D0 day (so throughout the night time previous ECB press-conference). The value motion is identical for the DAX and the STOXX 50 Index, too.

The fairness curves for D0 Open-to-Shut periods in each indices reveal an antagonistic market response to ECB bulletins, indicating that markets are likely to react negatively to ECB coverage revelations.

We will summarise the general annualised (yearly) return for all abovementioned easy technique variations within the following desk:

Why do the markets react in another way to ECB bulletins (pre-ECB drift) than to FED bulletins (FOMC assembly drift)? We have now our personal speculation, and it’s related to the position of worldwide traders within the European markets. We’ll get to it, however first, let’s analyze how the US-listed European equities carry out throughout the pre-ECB drift.

U.S. ETFs Evaluation of European Indices

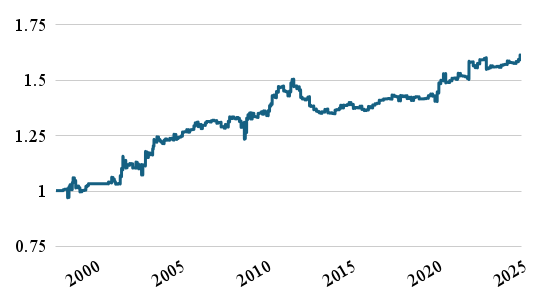

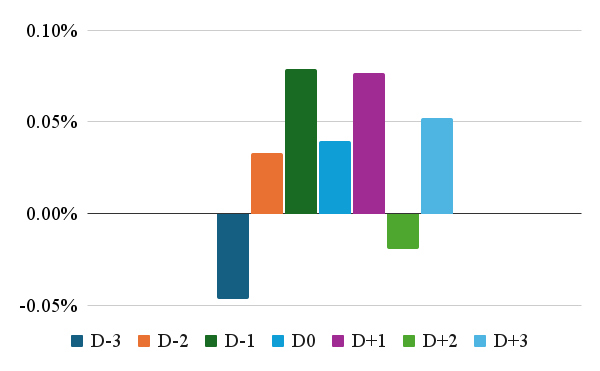

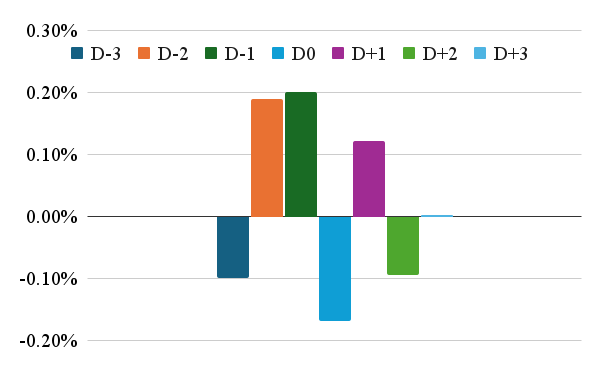

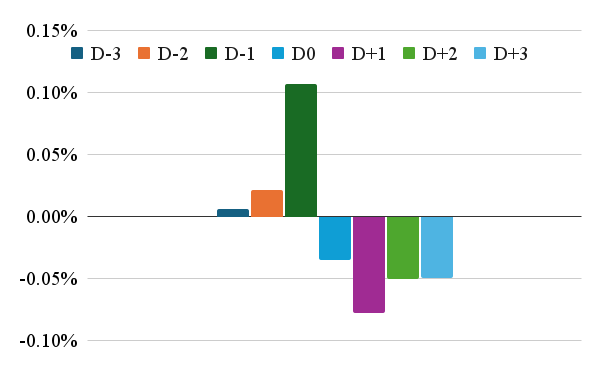

Within the following charts, we current histogram of common day by day efficiency over the D-3 to D+3 days and a fairness curves for the U.S. ETFs – FEZ, VGK, EWG, and HEDJ, which put money into European inventory indices.

As could be seen, these distributions just about mirror our evaluation about European inventory indices and observe the identical efficiency distribution patterns.

Nonetheless, it’s essential to think about that the US ETFs shut buying and selling at 4pm New York time, which is 10pm Paris/Berlin time. So D-1 efficiency bar for the US investor begins at 4pm NY (10pm Berlin) on D-2 and ends at 4pm NY (10pm Berlin) time. Why it’s essential? In case you are a US-based investor, you commerce within the US hours and need to keep away from the ECB charge determination; you may’t maintain the ETFs in a single day. You could promote them on D-1 shut because the ECB charge determination is introduced on D0 day within the morning when the US market continues to be closed.

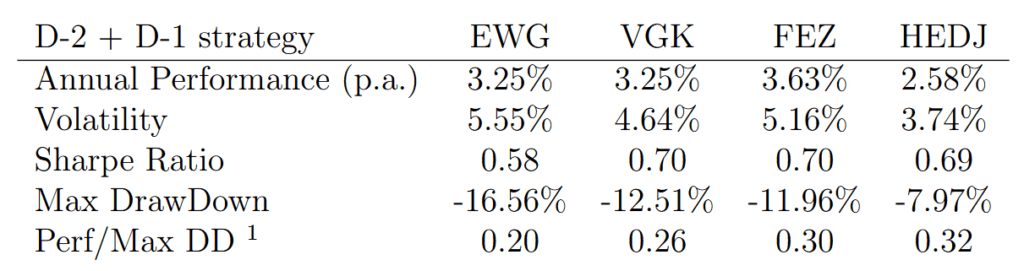

How would the cumulative efficiency of such a easy technique seem like?

As US traders, we don’t want to carry the ETF only for sooner or later; we are able to even have the place for two days previous the bulletins; that is how the efficiency and return-to-risk traits would seem like:

1 Calmar Ratio

Nonetheless, why do we’ve the “pre-ECB drift” and never the “ECB drift” on day D0 itself? We’ll go away the precise financial forces in play for different analysts nonetheless our idea is that there are behavioral biases in play. Probably the most possible clarification is that US institutional traders front-run the announcement and unwind their longs the day earlier than the assembly on the shut of the US session for the reason that ECB announcement launch is scheduled in pre-market hours, exterior of the common buying and selling session in America. Energetic merchants and traders could also be prepared to danger holding positions a couple of hours and even minutes earlier than the FED announcement however will not be so prepared to do it for the ECB. The European Central Financial institution doesn’t have the identical place as the worldwide liquidity provider because the FED. So, from the attitude of the US dealer or investor, it is sensible to take a position a little bit (the day earlier than). Nonetheless, it doesn’t make sense to carry the dangerous place in a single day and rebalance portfolio (or minimize danger) throughout morning hours when the US markets are nonetheless not open.

Can we verify our speculation? Circuitously (we didn’t ask US merchants about their emotions concerning the ECB), however we are able to calculate the unfold between EWG and SPY ETFs and take a look at it. The distribution of the efficiency for days D-3 to D+3 for the unfold itself ought to give us some understanding of whether or not the pre-ECB drift is attributable to the efficiency of the worldwide inventory markets or simply by the European value motion itself. Within the following chart, we are able to clearly see the build-up within the efficiency of the unfold in D-2 and D-1 days and the unfavorable efficiency from days D0. This implies that the pre-ECB drift is basically only a European-only phenomenon. Nonetheless, it additionally suggests, that exterior (non-European) traders might actually drive the drift itself.

In conclusion, our brief research contributes to understanding how central financial institution actions, significantly these of the ECB, affect monetary markets. Buyers can develop extra knowledgeable methods to capitalize on market actions round ECB coverage bulletins by figuring out and quantifying the pre-ECB impact. Moreover, policymakers can use these insights to refine communication methods and higher handle market expectations. The findings additionally spotlight the significance of contemplating behavioral biases and institutional investor actions in understanding market dynamics.

Our advised technique variants, which entails holding positions D-2 and D-1 days earlier than ECB conferences, demonstrates potential for producing constructive returns. Nonetheless, it’s essential to constantly monitor and adapt this technique as market circumstances evolve, guaranteeing it stays efficient in capturing the pre-ECB drift. Furthermore, incorporating behavioral finance insights and understanding institutional traders’ position in shaping market reactions can additional refine this method, resulting in extra subtle funding selections.

Future analysis may discover how these results range throughout financial circumstances and coverage environments, offering a extra nuanced view of central financial institution affect on monetary markets. Moreover, integrating superior econometric fashions and machine studying strategies may improve the predictive energy of such analyses, providing extra sturdy funding methods and coverage suggestions.

Are you on the lookout for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you need to study extra about Quantpedia Premium service? Examine how Quantpedia works, our mission and Premium pricing provide.

Do you need to study extra about Quantpedia Professional service? Examine its description, watch movies, evaluation reporting capabilities and go to our pricing provide.

Are you on the lookout for historic knowledge or backtesting platforms? Examine our listing of Algo Buying and selling Reductions.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a buddy