")

primeimages

We use the time period danger all too casually, and the time period uncertainty all too not often.– John Bogle

In 1969, IBM directed San Jose venture supervisor Kenneth Haughton to develop a “direct entry storage facility” that matched the efficiency of the high-end IBM 3330 system at a worth enticing to low-end System/370 clients. The IBM3340 onerous disk drive (HDD), which started transport in November 1973, launched a brand new, low-cost, and low-load design with learn/write heads that landed on lubricated disks, establishing what turned the main HDD know-how. Primarily based on the unique specification of a system with two spindles, every holding a 30 MB disk, Haughton famous, “If it is a 30-30, then it have to be a Winchester,” referring to the .30-30 Winchester rifle cartridge. Business observers recognized this new “Winchester head” as one of many 4 most important developments in mass storage. The IBM Mannequin 3350, launched in 1975, remodeled the information module right into a non-removable head disk meeting with a 317 MB capability, a design that some name “the actual Winchester,” which has remained the elemental HDD packaging idea to today.1

From 1977 to 1984, enterprise capital corporations invested almost $400 million in 43 Winchester disk drive producers throughout 51 completely different financing rounds, with 21 labeled as start-up or early-stage investments. Most of this funding, $270 million, occurred in 1983 and 1984. Throughout this era, the onerous disk drive business skilled fast development, with OEM market gross sales rising from $27 million in 1978 to $1.3 billion in 1983, and anticipated to succeed in $2.4 billion in 1984 (an 84% improve). Projections additionally forecasted that the market would surpass $4.5 billion by 1987. The passion in enterprise capital and inventory markets for Winchester disk drive producers, pushed by optimistic business forecasts, masked a phenomenon later generally known as “capital market myopia.” Fundamentals sharply declined in late 1984, with the mixed market worth of twelve key disk drive corporations dropping from $5.4 billion to $1.4 billion.2

Particular person funding selections, which appear rational on their very own, can usually collectively result in poor outcomes. When seen alone, every funding choice seems justified. Collectively, these selections kind a recipe for funding ache. Buyers, fixated on potential features, overlook clear warning indicators, on this occasion, the overvaluation and overcrowding of the Winchester disk drive business. Market contributors ought to have foreseen the sector’s collapse, however the concern of lacking out (FOMO) is a timeless and compelling emotion. This sample often repeats itself, pushed by the “better idiot concept,” an funding idea suggesting that an asset’s worth might be pushed increased by speculative demand, even when its intrinsic worth is questionable. Buyers all the time consider they will promote the “funding” later to a “better idiot” at the next worth. It depends on the belief that there’ll all the time be somebody keen to pay extra, whatever the asset’s basic value.

The increase and bust of the Winchester disk drive business from 1977 to 1984 parallels the explosive development of the synthetic intelligence (AI) and knowledge heart markets of right now. The worldwide AI semiconductor market was valued at $56 billion in 2024 and is projected to succeed in $232 billion by 2034, a compound annual development price of 15.2%. Information heart demand for AI workloads has surged, with Nvidia reporting a 73% year-over-year improve in knowledge heart income to $39.1 billion within the first calendar quarter of 2025. Just like the Winchester disk drive of fifty years in the past, hyperscalers (large-scale cloud service suppliers) and GPU cloud suppliers, resembling CoreWeave (CRWV), are quickly increasing their capability to satisfy business forecasts. Nvidia’s (NVDA) dominance in AI GPUs has pushed its fairness market capitalization to $3.9 trillion, equal to the market capitalization of all the German inventory market.

Within the 1985 paper “Capital Market Myopia,” written by William Sahlman and Howard Stevenson, the authors analyze the increase and bust of the Winchester disk drive business. They observe that winners and losers are decided by one’s skill to navigate irrational exuberance brought on by collective funding selections that ignore business fundamentals. The clear winners had been the enterprise capitalists who invested early in disk drive corporations and funding bankers who facilitated the rising business’s preliminary public choices (IPOs). Early traders reaped huge earnings by capitalizing in the marketplace’s euphoria. For instance, Seagate’s enterprise capitalists invested $1 million for 17% of the corporate, which was value $32 million post-IPO in 1980, when Seagate’s market valuation reached $185 million—a ridiculous valuation a number of of eighteen instances trailing twelve-month gross sales. Funding bankers profited from over $800 million of business underwriting charges. Winners additionally included founders and executives of disk drive corporations who leveraged the new IPO market to promote shares at peak valuations. Curiously, the authors praised firm executives who raised cash at wealthy valuations, because the business required heavy exterior capital attributable to excessive fastened property and dealing capital wants.

The Winchester disk drive bubble additionally created many losers, notably traders who purchased disk drive shares in 1983 at peak valuations. These traders confronted huge losses when market values collapsed 74% from $5.4 billion to $1.4 billion by late 1984. Irrational exuberance and the “better idiot concept” neglected business overcrowding, with over seventy disk drive corporations competing for market share, and unsustainable fundamentals. The disk drive business, and by extension, U.S. technological competitiveness, additionally suffered because of this. This funding sample will ultimately apply to widespread sectors in right now’s market, together with AI semiconductors, knowledge facilities, renewable vitality, and battery storage, the place early traders profit from the “better idiot concept.”

A yr in the past, the thrill surrounding AI confronted a harsh actuality test on Wall Avenue. Goldman Sachs’ head of fairness analysis, Jim Covello, questioned whether or not corporations planning to speculate $1 trillion in constructing generative AI would ever see a return on their funding.3 Enterprise capital agency Sequoia estimated that know-how corporations wanted to generate $600 billion in further income to justify their elevated capital spending in 2024 alone, about six instances greater than they had been more likely to produce. These warnings sparked the primary check of funding sentiment. Income from finish clients, who hoped to profit from this new know-how, was minimal—there aren’t any definitive generative AI “killer apps” in the marketplace but. A yr later, main AI shares hit new all-time highs. Overcoming worries that began earlier within the yr with the low-cost Chinese language competitor DeepSeek (DEEPSEEK), Nvidia rebounded to set a file excessive, including $1.5 trillion in inventory market worth from its April low, whereas Microsoft (MSFT) added $1 trillion in market worth. Nonetheless, little has modified in AI’s broader income prospects since final yr’s warnings. The optimism and hype stay as robust as ever, and it’s nonetheless tough to see the place future returns will justify the large capital investments in AI, a minimum of within the close to time period.

Resurgent optimism ought to come as no shock. In any case, in America, one can stroll right into a on line casino and wager one’s life financial savings on purple or black. Whether or not it’s a bug or a function, there’s something to the American spirit that appears to sit down extra comfortably with funding danger than wherever else. Naturally, Wall Avenue takes full benefit of our tendency to take dangers. Wall Avenue is presently launching exchange-traded funds (ETFs) focusing on speculative property like smaller cryptocurrencies, meme cash (e.g., Dogecoin, $TRUMP), and even corporations tied to “reverse-engineered alien know-how,” pushed by retail traders’ urge for food for unique investments. The surge in ETF filings, together with a UFO Disclosure AI-Powered ETF, acknowledges Wall Avenue’s mastery of the “better idiot” concept.4

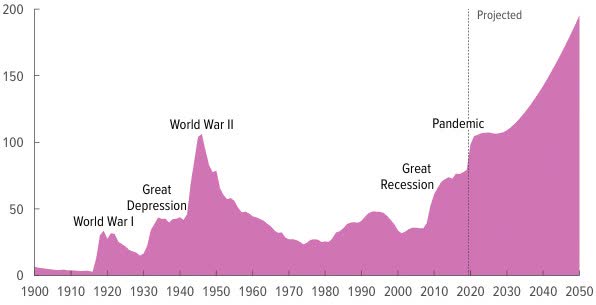

One sometimes associates capital market myopia with microeconomics, however one wonders if there’s some software to the macroeconomic image. There’s little doubt that america is a going concern, however its monetary operations do elevate questions. The U.S. authorities obtained roughly $4.9 trillion in income however spent $6.8 trillion. Regardless of the big hole between working income and bills, the U.S. authorities funds itself with out challenge. The first considerations deal with the long run. The U.S. Treasury owes $37 trillion, gross, together with $9 trillion to international holders of U.S. debt. Brett Loper, government vp for coverage on the Peter G. Peterson Basis, lately summarized the state of fiscal coverage, “Even holding Medicare on autopilot and Social Safety on autopilot and Medicaid on autopilot, not making any modifications, rising or lowering the price of these packages, you’re an quantity of debt rising by $22 trillion over the subsequent ten years simply to fund the federal government. You’re speaking about the price of curiosity funds on the debt doubling. Curiosity funds this yr are going to value greater than all the quantity we spend on nationwide protection, and but they’re going to double over the subsequent ten years. For those who consider curiosity funds on excellent Treasury debt as a program of the federal authorities, it’s the fastest-growing program within the federal authorities.”5

Federal debt held by the general public is projected to equal 195% of gross home product (GDP) in 2050, and the deficit is projected to equal 13% of GDP. Supply: CBO

Every President and member of Congress makes funds selections, which appear rational on their very own, however collectively usually result in a poor final result. The U.S. Congressional Price range Workplace gives nonpartisan budgetary and financial evaluation to assist Congress in its legislative and budgetary selections. Nonetheless, it additionally allows these particular person funds selections by making no allowances for wars or financial recessions—the CBO assumes that authorities borrowing prices will stay at rates of interest ranging between 3.4% and three.6% indefinitely. Credit standing company Moody’s lastly joined Customary & Poor’s and Fitch Scores in downgrading the nation’s credit standing on Might 16. To not fear, although, the S&P 500 closed up on that day.

As demonstrated in the course of the 2008 monetary disaster, credit score companies are typically backward-looking. The capital markets already know america just isn’t rated AAA. Insurance coverage on U.S. sovereign credit score trades on the similar degree as Greece and Italy. Critically, credit standing companies play an important position in perpetuating the “better idiot” concept by sustaining the narrative that U.S. monetary property are precisely priced at their intrinsic worth. Wall Avenue exploits the credit score company narrative to promote funding merchandise that always lack factual or logical integrity. In his masterpiece ebook The Value of Time, Edward Chancellor gives a scathing abstract of the present funding panorama:

“We have now come to reside in a managed atmosphere, with its faux cash, faux rates of interest, faux financial system, faux jobs, and faux politicians. Our bubble world is sustained by a mix of passive acquiescence and highly effective vested pursuits. It’s a 24/7 present with a worldwide viewers. Since danger is managed, we’ve nothing to concern. Any departure from the bubble threatens a disaster. Excessive measures are adopted: adverse rates of interest, limitless quantities of quantitative easing. An excessive amount of is at stake to let the bubble burst.”6

The duty of the investor is to discern worth amidst the assorted narratives propagated by Wall Avenue, acknowledge the disconnect between hope and actuality, perceive why it exists, after which uncover the reality. The investor’s goal is to capitalize on the disparity between worth and worth. Sadly, most traders lack the temperament to withstand the siren’s name to invest. Anyone who operates within the funding business lengthy sufficient acknowledges that market conduct usually appears to come back straight out of Alice in Wonderland. In few different areas of on a regular basis exercise is one so usually invited to consider that what appears “good” is actually “unhealthy,” and vice versa. Declaring “Liberation Day” for import tariffs is unhealthy, however deferring any selections for ninety days is sweet; huge deficit spending is unhealthy for the nation however nice for company revenue margins; the Federal Reserve rising rates of interest to fight inflation is unhealthy however reducing rates of interest due to a stagnant financial system is sweet.

Not surprisingly, this Alice in Wonderland conduct tends to baffle unusual traders, reinforcing the notion that there’s some mystique about monetary markets that the unusual investor can’t comprehend. Including to the confusion is that Wall Avenue purposely obscures the distinction between an analyst and an advocate. To an analyst, being flawed is disappointing, however it additionally presents a possibility to be taught—a necessary component in a suggestions loop of steady enchancment. Not so for the advocate. The advocate ties their revenue motives to a particular final result and feels compelled, whether or not consciously or not, to rationalize away or assault inconvenient realities. It’s advocacy when every second of unfavorable market worth motion is met with a cacophony of requires central banks and politicians to behave. In reality, there isn’t a thriller to the funding course of. Benjamin Graham offered traders with a path over seventy-five years in the past to navigate the funding panorama. Graham, thought of the daddy of worth investing and writer of the 1949 ebook “The Clever Investor,” offered a easy but elegant set of ideas for investing.

Graham usually targeted on deciding on securities representing what he deemed a sound enterprise, notably one with a robust steadiness sheet. Whereas the enterprise could also be sound, Graham knew the market couldn’t be relied upon to worth it accurately at any given cut-off date. In instances of market stress, sound corporations can simply fall prey to a panic that envelops the broader market and captures investor psychology. Conversely, in instances of excessive confidence, such corporations could also be seen as ‘boring’ when fast-paced development is all traders care about. Graham believed the important thing to making sure the scales had been tipped in his favor lay in ensuring that, irrespective of how sound the corporate, it ought to by no means be bought at too excessive a worth – a consideration many traders, notably throughout instances of speculative extra, overlook. Graham termed this distinction between what he paid for a inventory and what he believed its true, intrinsic ‘worth’ to be because the ‘Margin of Security.’

Though the paper “Capital Market Myopia” concerning the Winchester disk drive business was printed 9 years after Graham’s loss of life, he would have instantly acknowledged this era as a traditional case of speculative extra pushed by irrational exuberance, a phenomenon he repeatedly cautioned towards. The Winchester disk drive business’s 74% crash exemplified his warnings about Mr. Market’s irrationality and the risks of hypothesis. Graham’s funding ideas stand the check of time. In 1974, Forbes journal interviewed a number of grizzled veterans of the Wall Avenue funding neighborhood, contemporaries of Graham.7 That they had lived by each good instances and unhealthy, gaining a perspective that solely age and expertise can present. Every had been fairly profitable of their lengthy funding careers. They had been all fundamentalists who bought stable corporations in stable industries with stable administration and stable steadiness sheets.

Whereas not one of the veteran traders allotted all their capital to widespread shares, all of them possessed the emotional self-discipline to experience by many years of inventory market volatility. At age 71 (1974), Joseph Nye retired from Wall Avenue when he offered his New York Inventory Alternate seat for $205,000 in 1972, however didn’t retire from investing. Nye mirrored on his funding profession, “, most individuals don’t know what stands behind their funding in widespread shares. We do. We’re cautious to the purpose of thoroughness.” Bradford Story, who graduated from Yale College in 1923, and was the final surviving founding accomplice of Brundage, Story & Rose, a conservative funding counseling agency at 90 Broad Avenue, famous that “We take the dangers of the capitalist, however by no means the dangers of the Wall Avenue man. The capitalist takes industrial dangers, not monetary dangers.” In different phrases, Story seemed for robust corporations, not inventory market quotations. When the article’s writer requested Story about quarterly earnings as an funding information, he replied, “As soon as you purchase earnings, you develop into an inexpensive little guesser.”

Over the many years, Nye and Story watched lots of their colleagues get into bother and go beneath. Males like Nye and Story accepted their funding errors with dignity however took the chance to be taught from their errors. They had been realists fairly than optimists or pessimists. In conventional societies, concluded the Forbes article, the younger be taught from their elders. Against this, Wall Avenue tends to take heed to youth, not age. Youth is ok when there are considerable alternatives. Youth possess the vitality and drive to take full benefit of those potentialities, however the younger can provide no steering when instances develop powerful—it’s a new expertise for them. Then the statesmen, the village elders, the “grandfathers” come into their very own.

The USA has been blessed with an abundance of assets and prosperity for thus lengthy that it’s nearly unimaginable for an investor right now to ponder the funding panorama of the Nineteen Thirties. One factor repeatedly emphasised by the outdated funding veterans was the dearth of money to purchase shares after they traded at discount costs. No person had any cash. The mix of a 90% market decline and widespread financial institution failures within the early Nineteen Thirties resulted within the destruction of individuals’s financial savings. The banks that didn’t fail froze their clients’ financial savings accounts and imposed every day withdrawal limits on the amount of cash a buyer may withdraw. In some circumstances, it was as little as 5% of the cash of their account. Some had been so determined for money that they offered their financial institution passbooks (a file of their account, if one is sufficiently old to recollect) at 50% or much less of the quantity of their account to get money. And that was not unusual—the newspapers offered every day quotes on financial institution passbooks.

The funding elders additionally famous that folks did not be taught from the 1929 crash. They knew of many Wall Avenue colleagues who misplaced every little thing within the 1929 crash, solely to repeat the identical mistake 4 or 5 years later. A number of of their colleagues purchased shares close to the lows of the Nice Despair, rode the restoration, and made a small fortune once more. However fairly than promote, they received grasping. They maxed out their accounts on margin to purchase extra shares, solely to look at the market flip and wipe them out once more. The ability of desperation and greed over rational funding selections is timeless and onerous to beat. Evolution has hardwired these feelings into people. A mindset centered on capital preservation is essential for surviving and prospering over many many years of investing within the capital markets.

The ideas of conservative funding apply whether or not one buys actual property, shares, bonds, or corporations like these producing Winchester disk drives in 1984, or the generative AI corporations of right now. A cautious evaluation of the corporate’s fundamentals is important, with the protection of 1’s principal all the time on the forefront of any funding choice. In search of abnormally excessive returns invitations better danger and hypothesis. In Benjamin Graham’s writings, he repeatedly emphasised that avoiding catastrophic losses was essential for any investor aiming to attain regular compounded returns all through their funding profession. Such losses place the investor in an unenviable place; they attempt to chase efficiency to recuperate to their earlier degree of capital.

Throughout his 2005 graduation speech at Stanford College, Steve Jobs used the phrase “You’ll be able to’t join the dots trying ahead; you may solely join them trying backwards” to convey that life’s path and the importance of occasions usually solely make sense on reflection. When making selections, whether or not about profession, schooling, or private pursuits, Jobs knew he couldn’t predict with certainty how these selections would result in future outcomes. As a substitute, readability emerges later, when one displays on how seemingly unrelated experiences, selections, or errors match collectively to form one’s life journey. Jobs illustrated this together with his personal life—he dropped out of Reed School and took a calligraphy course, which appeared aimless on the time however later influenced Apple’s deal with typography and design.

Jobs suggested the brand new graduates to belief the method and comply with their curiosity and instinct. The “dots” signify key moments or selections that ultimately align in methods one can’t foresee. As an investor, one should make the very best selections primarily based on the knowledge presently obtainable. In hindsight, every little thing usually appears logical, however trying forward is all the time stuffed with uncertainty. Funding survival requires a disciplined, conservative strategy. Funding errors can show fairly painful, however in addition they provide a possibility to replicate and be taught. Profitable traders should stay hungry to be taught, to learn, to hear, and attempt to join the “dots.”

With variety regards,

St. James Funding Firm

Footnotes

1https:// www.computerhistory.org/storageengine/winchester-pioneers-key-hdd-technology/.

2William Sahlman and Howard Stevenson, “Capital Market Myopia,” Journal of Enterprise Venturing, Vol. 1, 1985, pages 7 – 30.

3Will the $1 trillion of generative AI funding repay?

4https://www.sec.gov/Archives/edgar/knowledge/1771146/000121390025009523/ea0229673-01_485apos.htm

5“As soon as Stated, Can’t Be Unsaid” Grants Curiosity Fee Observer, Vol.43, Might 9, 2025.

6Edward Chancellor, The Value of Time: The Actual Story of Inter est, New York, Atlantic Month-to-month Press, 2022.

7“The Grandfathers,” Forbes, September 1, 1974, Pages 28 – 31.

St. James Funding Firm

We based the St. James Funding Firm in 1999, managing wealth from our household and mates within the hamlet of St. James. We’re privileged that our neighbors and mates have trusted us to speculate alongside our capital for twenty years.

The St. James Funding Firm is an unbiased, fee-only, SEC- registered funding Advisory agency that gives personalized portfolio administration to people, retirement plans, and personal corporations.

Disclaimer

Info contained herein has been obtained from dependable sources however just isn’t essentially full, and accuracy just isn’t assured. Any securities talked about on this challenge shouldn’t be construed as funding or buying and selling suggestions particularly for you. You will need to seek the advice of your advisor for funding or buying and selling recommendation. St. James Funding Firm and a number of affiliated individuals could have positions within the securities or sectors beneficial on this publication. They could, due to this fact, have a battle of curiosity in making the advice herein. Registration as an Funding Advisor doesn’t suggest a sure degree of talent or coaching.

To our shoppers: please notify us in case your monetary state of affairs, funding aims, or danger tolerance modifications. All shoppers obtain a press release from their respective custodian on, at minimal, a quarterly foundation. If you’re not receiving statements out of your custodian, please notify us. As a shopper of St. James, it’s possible you’ll request a replica of our ADV Half 2A (“The Brochure”) and Kind CRS. A replica of this materials can also be obtainable on our web site at www.stjic.com. Moreover, it’s possible you’ll entry publicly obtainable details about St. James by the Funding Adviser Public Disclosure web site at www.adviserinfo.sec.gov. You probably have any questions, please contact us at 214-484-7250 or data@stjic.com.

Click on to enlarge

Unique Submit

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.

Q2 2025 Earnings Name Transcript")